Introduction

Money has always moved. But in 2026, it moves faster, smarter, and across more borders than at any point in human history. The global payments landscape — once a maze of correspondent banks, paper trails, and three-to-five business day delays — has been fundamentally reimagined. Today, a startup in Nairobi can collect payments from a customer in Oslo in seconds. A manufacturer in Shenzhen can settle invoices with a distributor in São Paulo before the end of a business day. A freelancer in Manila can receive a wire from a client in Toronto without losing a quarter of it to fees.

This transformation is not accidental. It is the product of a decade of relentless innovation, regulatory evolution, open banking mandates, and the quiet but powerful rise of fintech infrastructure companies working behind the scenes to rewire how value flows across the world.

For business leaders, investors, and entrepreneurs, understanding the architecture of modern global payments is no longer optional — it is a strategic imperative.

The Scale of the Opportunity

The global payments industry processed over $3.4 trillion in revenue in 2025, according to industry analysts, and is projected to surpass $4.5 trillion by 2030. Cross-border payments alone — encompassing trade finance, remittances, B2B transfers, and e-commerce settlements — represent a market exceeding $250 trillion in annual transaction value.

Yet despite these staggering numbers, the system has historically been riddled with friction. High fees. Opacity. Slow settlement times. Fragmented regulatory regimes. Currency risk. These pain points have long been accepted as the price of doing business globally. But that acceptance is rapidly eroding as a new generation of payment solutions delivers what was once thought impossible: fast, affordable, transparent, cross-border money movement at scale.

The Major Forces Reshaping Global Payments

1. Real-Time Payment Networks

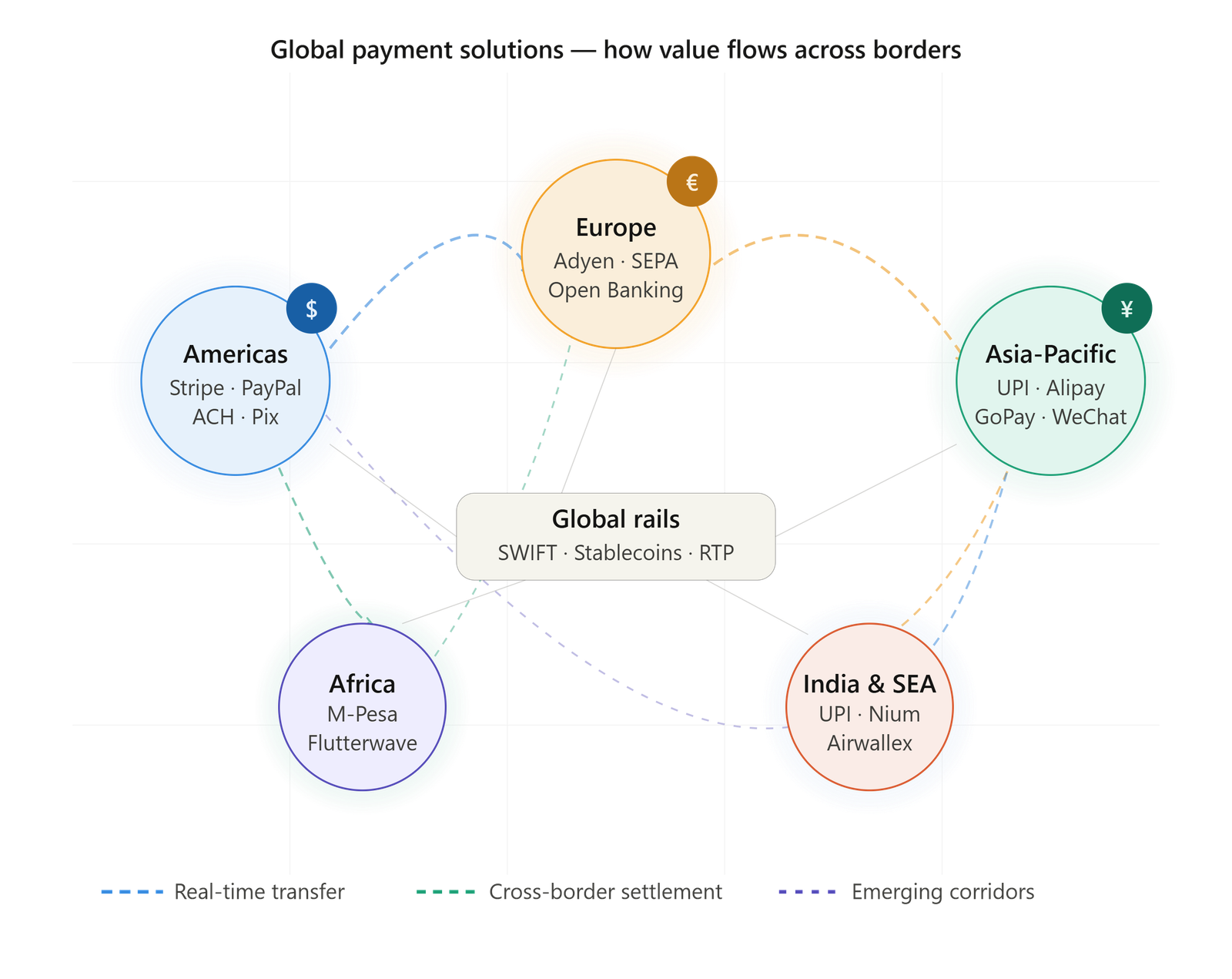

Perhaps the single most significant development in global payments over the past five years has been the proliferation of real-time payment (RTP) infrastructure. Countries around the world have built or upgraded domestic instant payment rails, and these networks are increasingly being linked together.

India’s Unified Payments Interface (UPI) is the gold standard. Processing over 18 billion transactions per month, UPI has become a model that other nations are actively replicating or connecting to. Singapore’s PayNow, Brazil’s Pix, the European Union’s SEPA Instant, and the United Kingdom’s Faster Payments are all part of a growing ecosystem of instant payment systems. The G20’s cross-border payments roadmap has made the interlinking of these systems a global priority, with pilot corridors between countries already operational.

For businesses, this means that the expectation of real-time settlement — once a domestic luxury — is becoming the global norm.

2. Open Banking and API-Driven Infrastructure

Open banking regulation has unlocked a new layer of payment innovation. By requiring banks to expose customer data and payment initiation capabilities through standardized APIs (with customer consent), regulators in the EU, UK, Australia, Brazil, and beyond have enabled a new class of fintech companies to build directly on top of the banking system.

The result is a generation of account-to-account (A2A) payment solutions that bypass card networks entirely, reducing costs dramatically for merchants. Companies like Plaid, TrueLayer, Tink (now part of Visa), and Yapily have built the connective tissue between banks and businesses, enabling seamless payment initiation, account verification, and data aggregation across dozens of markets from a single integration.

For CFOs and treasurers, open banking has made it possible to manage multi-currency cash positions, automate reconciliation, and sweep funds between entities in real time — capabilities that once required expensive treasury management systems and dedicated banking relationships.

3. The Rise of Payment Orchestration

As businesses expand globally, they inevitably face a complex matrix of payment methods, currencies, local regulations, and consumer preferences. A payment method beloved in Germany (bank transfers) may be irrelevant in Indonesia (where digital wallets like GoPay and OVO dominate). A checkout experience optimized for the United States will convert poorly in Brazil, where Boleto Bancário and Pix split the market with credit cards.

Payment orchestration platforms solve this problem by sitting above multiple payment service providers (PSPs), gateways, and acquirers, intelligently routing transactions to maximize authorization rates, minimize costs, and ensure local compliance. Platforms like Spreedly, Primer, Paydock, and Gr4vy allow businesses to connect once and access a global network of payment rails, adapting dynamically based on the customer’s location, device, and transaction profile.

This “smart routing” approach has proven to be a significant competitive advantage. Businesses using orchestration layers report authorization rate improvements of 3–8%, which at scale translates directly to millions in recovered revenue.

4. Embedded Finance and the Invisible Payment

One of the most profound shifts in the payments landscape is the gradual disappearance of the payment itself as a distinct step in the customer journey. Embedded finance — the integration of financial services directly into non-financial platforms and workflows — is making payments increasingly invisible.

Ride-hailing apps charge you without a checkout. E-commerce platforms offer instant financing at the point of purchase. B2B software platforms enable invoice financing, supplier payments, and expense management without ever leaving the workflow. The payment has become a feature, not a destination.

Enablers of this trend — companies like Stripe, Adyen, Rapyd, and Nium — offer modular infrastructure that allows any software company to become a financial services provider. The market for embedded payments is expected to exceed $6 trillion in transaction value by 2028.

5. Stablecoins and Blockchain-Based Settlement

No discussion of global payments in 2026 would be complete without addressing the maturing role of stablecoins in cross-border settlement. While the broader cryptocurrency market has remained volatile, dollar-pegged and euro-pegged stablecoins have found genuine product-market fit in specific payments use cases.

For treasury teams managing multi-currency operations in markets with volatile local currencies, stablecoins offer a way to hold value and settle transactions in hard currency without relying on the traditional correspondent banking system. Firms operating in Latin America, Sub-Saharan Africa, and Southeast Asia are increasingly using USDC and USDT as a settlement layer between local currency conversions.

Major payment companies have taken notice. Visa and Mastercard now support stablecoin settlement on select networks. PayPal has launched its own stablecoin, PYUSD. Circle, the issuer of USDC, has built a cross-border payment network used by banks and fintechs across more than 180 countries.

Regulatory clarity — still evolving across jurisdictions — will determine how quickly this use case scales. But the direction of travel is clear: blockchain-based settlement rails are becoming a legitimate part of the global payments stack.

Key Players Defining the Global Payments Landscape

The global payments ecosystem is vast, but a handful of companies have achieved the scale, technology, and regulatory footprint to operate as true global infrastructure providers.

Stripe remains the developer-first payment platform of choice for businesses scaling internationally, offering coverage across 135+ currencies and a suite of financial services products built on top of its core payments infrastructure.

Adyen has staked its identity on the unified commerce thesis — one platform, one integration, for in-store, online, and mobile payments across markets. Its direct acquiring model gives it structural cost advantages and superior data insights.

Wise Business (formerly TransferWise) has democratized international transfers, offering mid-market exchange rates and transparent fees for businesses managing multi-currency payments and payroll.

Airwallex has built a global financial infrastructure platform specifically designed for modern businesses, offering multi-currency accounts, global cards, and local payment rails without the complexity of traditional banking relationships.

Nium operates as a global payments infrastructure provider for fintechs and enterprises, enabling real-time cross-border payments, card issuance, and local payment collections across 190+ countries through a single API.

Flutterwave and Paystack (now part of Stripe) have been pivotal in making Africa a viable payments market for global businesses, aggregating the continent’s fragmented payment methods behind clean APIs.

The B2B Cross-Border Challenge

While consumer payments have been largely transformed, B2B cross-border payments remain an area of significant friction and innovation. The B2B cross-border market is estimated at over $150 trillion annually, yet much of it still runs on legacy rails — SWIFT transfers, checks, and manual reconciliation — that introduce delays, errors, and high costs.

A growing cohort of companies is attacking this problem directly. Corpay (formerly FLEETCOR), OFX, Convera (formerly Western Union Business Solutions), and Ebury offer FX risk management, payment automation, and multi-currency accounts tailored to the needs of importers, exporters, and multinational SMEs.

Meanwhile, supply chain finance platforms are using payments as the mechanism to unlock working capital — allowing buyers to extend payment terms while ensuring suppliers receive early payment through third-party funding.

The trend toward virtual account numbers — unique bank account identifiers that can be assigned per supplier, per currency, or per transaction — is simplifying reconciliation dramatically, giving finance teams the ability to match payments to invoices automatically.

The Regulatory Dimension

Global payments do not operate in a regulatory vacuum. Compliance is arguably the most complex dimension of building or using a global payment solution, and it is growing more complex, not less.

Anti-Money Laundering (AML) requirements, Know Your Customer (KYC) obligations, sanctions screening, and local licensing requirements vary significantly across jurisdictions. The EU’s Payment Services Directive 3 (PSD3), currently in implementation, will introduce stricter fraud liability rules and stronger consumer authentication requirements. The Financial Action Task Force (FATF) continues to tighten Travel Rule requirements for virtual asset transfers.

For businesses, this means that choosing a payment partner is also a compliance decision. A provider’s regulatory footprint — the licenses it holds, the jurisdictions it can legally operate in, and the robustness of its compliance infrastructure — is a critical factor that is often underweighted in purchasing decisions.

What Business Leaders Should Know

For executives making decisions about their company’s global payments strategy, several principles have emerged as durable guidance:

Localize or lose the sale. Consumer research consistently shows that checkout abandonment spikes when preferred local payment methods are not available. Building a global payments stack requires genuine localization — not just currency conversion, but integration with the specific wallets, bank transfer schemes, and buy now pay later options that customers in each market expect.

Treat payments as a strategic asset. The best payment strategies are not set-and-forget infrastructure decisions. They are ongoing sources of competitive advantage — through better authorization rates, lower FX costs, faster settlement, and richer transaction data that informs product and pricing decisions.

Diversify your payment stack. Concentration risk in payments is real. A single PSP outage or pricing change can have material business impact. Building redundancy through multi-provider architectures or orchestration platforms is a form of operational resilience.

Invest in real-time visibility. The shift to real-time payments creates both opportunity and obligation. Businesses need treasury and finance systems capable of operating in real time — managing liquidity positions, reconciling transactions, and responding to payment events as they occur.

Looking Ahead: The Next Frontier

The trajectory of global payments points toward a future that is faster, more interconnected, and more intelligent. Several emerging developments are worth watching closely.

Central Bank Digital Currencies (CBDCs) are moving from concept to pilot in dozens of countries. If major economies launch interoperable CBDCs, they could fundamentally alter the cross-border settlement landscape, reducing reliance on correspondent banking and enabling programmable payments at the sovereign level.

AI-driven fraud prevention and payment optimization is becoming table stakes. Machine learning models that analyze hundreds of signals in real time — transaction history, device fingerprint, behavioral biometrics, network data — are now the primary line of defense against fraud, and the primary engine for maximizing payment authorization rates.

The unification of physical and digital commerce is accelerating. As the boundary between online and in-store shopping dissolves, payment systems that provide a unified view of the customer across all channels — and enable seamless transitions between them — will define the next era of commerce.

Conclusion

The global payments landscape in 2026 is not simply more efficient than it was a decade ago — it is structurally different. The infrastructure that moves money around the world has been rebuilt from the ground up, powered by real-time rails, open APIs, intelligent orchestration, and a new generation of fintech companies operating at global scale.

For businesses, this transformation is both an opportunity and a challenge. The opportunity: to transact globally with a speed, cost efficiency, and customer experience that was previously available only to the world’s largest corporations. The challenge: to navigate an ecosystem of extraordinary complexity, where the right stack of partners, platforms, and rails can be a source of competitive advantage — and the wrong ones can be a drag on growth.

The companies that will win in the global economy of the next decade are those that treat payments not as a cost center or a back-office function, but as a strategic capability — one that is continuously optimized, deeply localized, and built for the speed of modern commerce.